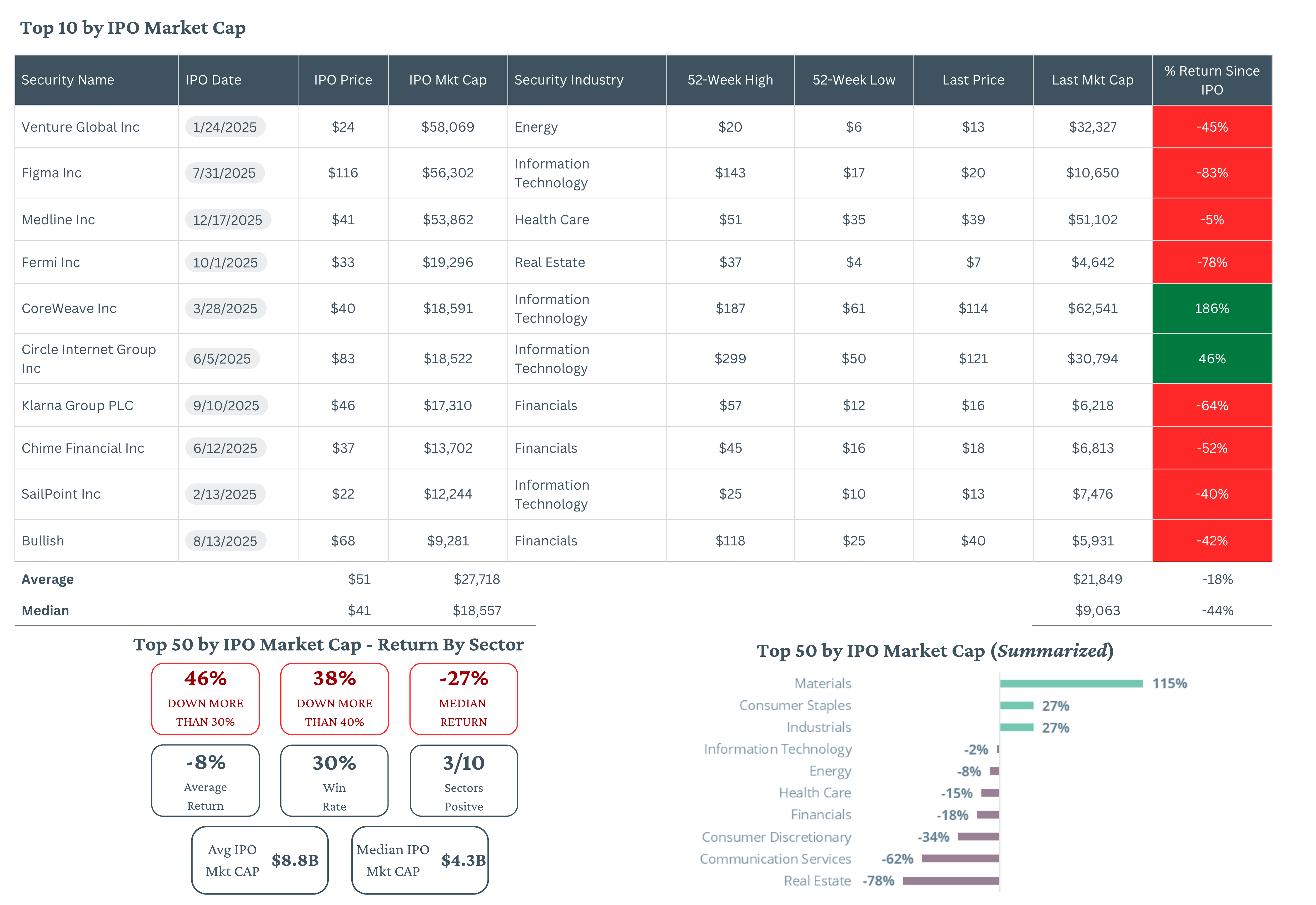

2025’s largest public market debuts have underperformed significantly. On average, the top 10 IPOs by market cap have lost 18%. 70% of them are down 40% or more! Only 2 of the top 10 companies have generated a positive return since listing, CoreWeave Inc (CRWV), and Circle Internet Group Inc (CRCL). The gap between private market enthusiasm and public market reality has rarely been more visible.

Looking beyond the top 10 IPOs of 2025, the story does not improve. The average return of the top 50 IPOs by market cap is -8%. 46% of the names are down more than 30%. Private market enthusiasm struggles to adapt to public market realities.

When markets get euphoric, we find it useful to zoom out and ask what history tells us about similar situations. Michael Mauboussin defines a base rate as a distribution of past outcomes for a specific reference class, a statistical baseline for how frequently certain results have occurred under similar conditions.¹

To use base rates effectively, you must be willing to fight your natural instincts. Our default mode of thinking, what Mauboussin and Nobel Prize winner Daniel Kahneman call the inside view, focuses on the unique details of a specific situation and builds predictions from those inputs alone. It is intuitive and immediate, but it is also prone to systematic bias. The opposite is what they call the outside view, setting aside what you think you know about a specific case and asking what the historical record says about situations like this one. It is the foundation of how we keep our investment views grounded in reality.

Kahneman illustrates the cost of not incorporating base rates in his book Thinking, Fast and Slow.² Working on a curriculum project, his team estimated completion would take two years. When asked how long similar projects had taken, the answer was seven to ten years and roughly 40% never finished at all. Kahneman called this the planning fallacy: forecasts that trend toward the best case precisely because similar situations were never consulted. In a market full of compelling stories, base rates are often the most important data point we have.

Back to the current situation, Altimeter’s Brad Gerstner has coined the term “quasi-public” for late-stage companies that have been shopped to so many large investors that price discovery has effectively already occurred before their formal listing. By the time the companies reach an IPO, the cap table is already populated with public market participants. This has real consequences for valuation, market expectations, as well as along with supply and demand dynamics once the stock begins trading.

While we don’t believe public market conditions create the feared risks of a Tech Bubble 2.0, we do see some concerning attributes in late-stage privates. In public markets, valuations have largely moved in line with earnings. Private market valuations are a different story. Venture capitalists are openly lamenting the competitive dynamics of getting into the most sought-after deals, often with little regard for valuation. Those dynamics don’t usually create attractive buying prices.

SpaceX is set to price on June 11th, making it the most highly anticipated IPO in a generation. An IPO that doesn’t fit our investment criteria. At a rumored valuation of $1.75 trillion on $18.7 billion in sales (94x trailing sales), the price requires an extremely optimistic view of the future, one that we think is being driven by enthusiasm for Elon Musk, space, and AI more than the underlying fundamentals of the company. Revenue growth decelerated in 2025 and the company is back to losing money. Given the valuations of SpaceX and Tesla relative to current fundamentals, we think they could present some of the largest risks when the secular bull market ends though we don't think we are close to the end yet.

The historical record supports our caution. Professor Jay Ritter of the University of Florida, widely known as "Mr. IPO," has compiled one of the most extensive IPO databases in existence, covering U.S. offerings from 1980 through 2024. His research shows that when a company’s price-to-sales ratio exceeds 40 at the time of listing, the average return over the following three years was a measly 3%, underperforming the market by 15%. From the first day’s closing price, which is closer to what retail investors obtain, the return was a negative 45%. SpaceX’s rumored valuation implies a price-to-sales ratio approaching 100 times. That is not a valuation that history has rewarded.³

We prefer to invest when expectations are low or when we have strong conviction that the market is underappreciating a company’s true potential. We think that opportunity exists elsewhere. Amazon, for example, whose low-earth-orbit satellite business competes directly with Starlink yet receives no recognition from the market. That is the type of asymmetry we look for at Patient Capital.

Source: Patient Capital Management Internal Analysis, Bloomberg data

The views expressed in this commentary reflect those of Patient Capital Management analysts as of the date of the commentary. Any views expressed are subject to change at any time, and Patient Capital Management disclaims any responsibility to update such views. There is no guarantee that market trends discussed herein will continue. These views are not intended to be a forecast of future events, a guarantee of future results or investment advice. Because investment decisions are based on numerous factors, these views may not be relied upon as an indication of trading intent on behalf of any portfolio. All investments involve risk of loss and past performance is not a guarantee of future results.

References to specific securities are for illustrative purposes only and are not indicated as a solicitation, or recommendation of any particular security or investment strategy.

Past performance is no guarantee of future results.

©2026 Patient Capital Management, LLC

Footnotes:

¹Michael Mauboussin, "The Base Rate Book," Credit Suisse Global Financial Strategies, 2016

²Daniel Kahneman, Thinking Fast and Slow(New York: Farrar, Straus and Giroux, 2011), Chapter 23

³Jay Ritter, University of Florida IPO Database, 1980–2024; as reported in "Sky-High I.P.O. Pricing Isn't Great for Real People," The New York Times, May 29, 2026.

Share